The cost of goods and services sharply increased in 2023. The most noticeable spikes were the cost of groceries, energy and vehicle-related costs. Drivers suffered up to a 67% rise in car insurance costs since 2023. Prices are still rising, which is a problem for drivers renewing in early 2024. To worsen the blow, the cost of vehicle fuel more than doubled during some months in 2023 compared to the previous year.

Most Brits have recently tightened their belts to offset rising costs but your car insurance premium just won’t budge. Car insurance should make up between 5% and 10% of our monthly budgets, but 27% now spend 10% or more on car insurance. Allocating more than a tenth of your budget on car insurance can put a strain on your finances.

Money Saving Expert explored some clever ways you can reduce your premium but are these too good to be true? Find out if you can really cut the cost of car insurance.

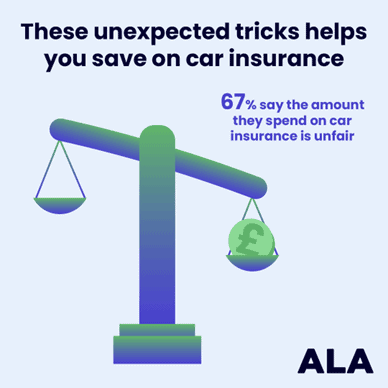

The legal requirement to have a policy in place to drive your car on UK roads means there’s always demand for car insurance. It’s easy to assume providers aren’t offering a fair car insurance price because of the demand for their service. In fact, 67% believe their car insurance premium is unfairly high – Shockingly, only 7% believe the cost is fair.

Car insurers only need to slightly undercut their competitors to attract new customers and often, the consequence of the lower price is suboptimal customer service or hidden admin fees. The good news is that, the Financial Conduct Authority regulates all motor insurance products. In 2023, the FCA penalised some insurers for undervaluing total losses. Trust in car insurers reaches an all-time low for some customers.

Motor insurers must submit their insurance value measures to the FCA every year. These measures include insurance claims frequencies, claims acceptance rates, average claim pay-outs and claims complaints as a percentage of total claims. The FCA reviews and evaluates the data before deeming that the products offer fair value to customers.

The rising cost of car insurance is mainly due to the steep surge in the price of car parts. This also means insurance companies are more likely to declare your car a write-off than in previous years, as it’s less economical to make repairs.

An increase in the national minimum wage increased the cost of labour, further increasing the cost of services. Insurers pass along the increased cost of parts and labour to the consumer. However, there could be a way to cut the cost of car insurance.

Reduce car insurance cost and keep the same cover

Your car insurer bases your premium on numerous factors such as age (young drivers pay more), driving experience, marital (yes, married couples pay less) and employment status, job title and no-claims discount. Also, counterintuitively, the fact that someone chooses comprehensive car insurance suggests they’re a more responsible driver. The more ways you can demonstrate you’re a low risk to the insurer, the lower your premium can be.

Money Saving Expert outlined the following nine ways to get cheap car insurance:

Never auto-renew

Quote 20-26 days before you need your policy to start

Add a responsible driver to the policy

Tweak your job title (legitimately)

Make sure you’re on the electoral roll

Check whether it’s cheaper to combine policies

Pay annually instead of in monthly instalments

Switch provider (no cancellation fee at renewal)

The FCA updated their regulations in 2022 to prevent insurers charging existing customers more than new customers for the same cover. Auto-renews might not pose a huge problem. Adding a responsible driver, tweaking your job title, and being on the electoral roll helps signal that you’re a lower risk. Combining policies and paying annually can enable benefits for loyal customers.

In theory, these methods can help you save money while keeping the same cover but which are the most effective strategies?

The tried and tested way to reduce car insurance costs

We asked Brits which methods they tried and whether they had any success at reducing car insurance premiums. We discovered that of those who’ve tried at least one of these techniques, 70% were successful.

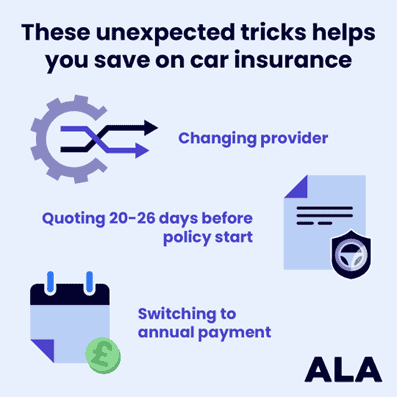

The most frequent methods attempted were changing provider (52%), quoting 20-26 days before policy start date (37%) and switching to an annual payment (22%). Yet, don’t overlook combining insurance policies (15%), adding an experienced driver (9%) and updating marital or job status (6%) as these could prove beneficial to you. Try as many of the following options as you can, prioritising options 1-3.

Changing provider (at renewal to avoid fees)

Quoting 20-26 days before policy start date

Pay for your car insurance annually

Combining insurance policies

Adding a safe driver to the policy

Tweaking job title

Updating marital status

Obviously, finding another provider offering the cheapest car insurance for the same cover is going to be an easy win. Also, despite the cash flow disadvantage, you should expect to save money by paying annually.

Quoting last minute won’t get you the best deal since you won’t have the time to shop around – you’ll likely accept the higher premium just to have a policy in place. On the other hand, most drivers will switch providers at renewal to avoid the admin fees, so quoting far in advance could suggest you’re not about to sign up – prices aren’t as competitive. Insurers are known to lower prices to attract customers who are weighing up their options before buying.

You can’t cheat your way to a lower premium but understanding the right signals and timings to consider could save you hundreds in the long run.