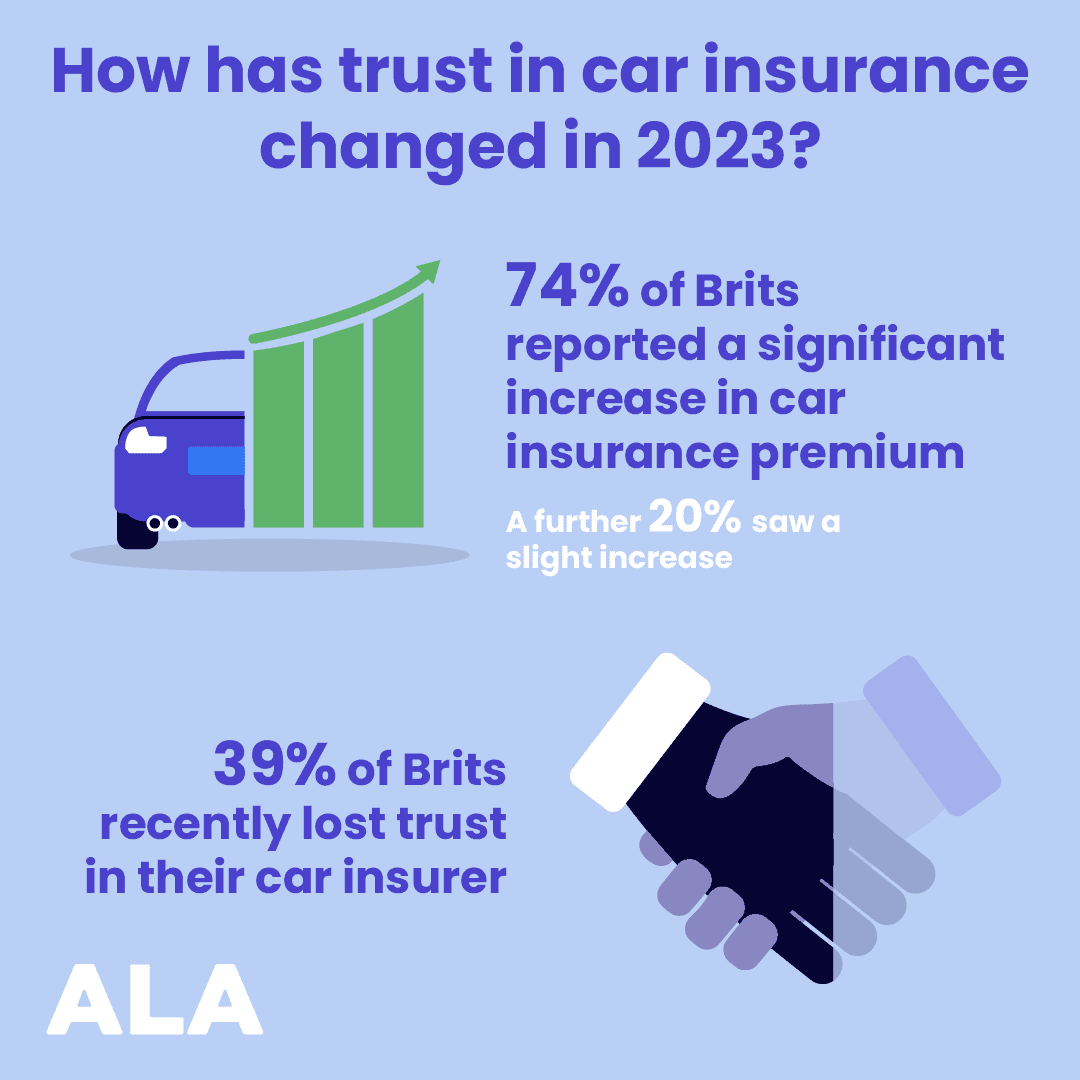

Most drivers say their car insurance premium has significantly increased. In fact, major insurers have raised their prices by 50-75% in recent months. With the cost of most things increasing during the cost-of-living crisis, it’s understandable that premiums rise too. The cost of car parts is soaring because of a lack of availability. Also, labour costs are affected by higher wages to offset inflation.

However, insurers are still turning a profit despite losing customers and having greater overheads. Opportunistic inflation could be costing you, meanwhile, your car insurer may not be completely transparent about their coverage.

We asked about how you feel about premiums, trustworthiness and car insurance cover, and we found interesting results. You could be missing out on vital protection against unfair decisions by your insurance provider.

Insurance providers don’t always have your best interests at heart when it comes to your coverage. Loopholes, exclusions, underpayments and hidden fees all help insurers profit when you need to make a car insurance claim. Insurance premiums are just part of the standard costs of owning a car but you should expect to get cover when you need it and to never be overpaying.

Despite most of you saying that your car insurance premium has significantly increased since the cost-of-living crisis, the majority trust their provider to offer the right insurance cover when they need it.

On the other hand, a large proportion has recently lost trust in their car insurance company (ALA, 2023). Hidden policy amendment fees, a lack of transparency and poor customer experience are some reasons why customers are doubtful.

With rising living costs and motor insurance premiums, it’s more important than ever to have the cover you need, receive a fair settlement if you need to make a claim and trust that your car won’t be written off without justification.

Major provider underpays total loss claims

In December 2022, the Financial Conduct Authority (FCA) investigated total loss claims from Direct Line and found that they had been undervaluing the vehicle market values for the past five years, meaning customers were receiving lower claim settlements than they should.

Despite one insurer being in the line of fire, undervaluations are increasing across the board. The average amount to be underpaid after a total loss is £616 and the number keeps rising despite a watchful eye from regulators.

Undervaluing a car after a total loss increases profits for insurance companies. Meanwhile, it leaves customers with a significant shortfall to cover. In fact, only 17% can afford even a like-for-like replacement with their car insurance settlement after a total loss (ALA, 2022).

Your motor insurer may declare total loss unfairly

In addition to underpayments after a total loss, major insurers may also write off vehicles without proper justification. A car is declared a total loss when the repair costs exceed a certain percentage of the market value of the vehicle, usually 60%. However, it’s increasingly common to see cars written for damages that don’t meet this criteria.

The increasing cost of parts combined with decreasing availability might contribute to insurers opting to write off the vehicle, rather than repair it. This leaves the driver needing a replacement vehicle when they could have had a repair on their current car. Again, most Brits can’t afford a like-for-like replacement with their insurance settlement alone, making it costly and inconvenient to write off a vehicle without proper cause.

Underpayments or unfair decisions help to offset increased insurance overheads and inflation. However, customers are also dealing with high insurance premiums – often without the premium service. Admiral’s profits were up 4% this year despite losing hundreds of thousands of customers, making it more important than ever to consider the trustworthiness of your motor insurer. Not every car insurer is shortchanging its customers but there are things you can do and be aware of to protect yourself in case your motor insurer doesn’t come in clutch. .

Firstly, investigate whether you’re overpaying for car insurance. Compare your car insurance quote with another provider and think about changing your cover. Admiral and Direct Line have been exposed as untrustworthy insurers but there could be many others.

Most of you didn’t know you could protect yourself against unfair decisions from car insurers. Protecting your investment with GAP insurance. Guaranteed Asset Protection insurance not only covers you against financial shortfall if your car is a total loss, it also acts as a safeguard against spurious underwriters making underpayments or possibly unfair decisions. ALA will top up your settlement, and unlike most other providers, we do our best to cover your shortfall, even if your car insurance settlement is low. What’s more, we can negotiate a fair settlement to ensure you aren’t shortchanged in the first place.

Four different types of GAP Insurance are available from ALA. Back to Invoice (BTI), Vehicle Replacement (VR), Contract Hire (CHG) and Agreed Value (AVG). These cover almost all types of vehicle – old cars, new cars, vans and even motorhomes. Depending on your policy, we’ll cover insurance shortfalls due to vehicle depreciation (VR, BTI & AVG) and vehicle finance (VR and BTI only), or outstanding lease payments and your initial deposit (CHG only). We’ll even cover up to £250 of your insurance excess to make things even easier.

A GAP insurance policy costs as little as a standard gym membership per month and, whilst the cover lasts for up to 4 years, the policy is a one-off cost which can also be split over ten months. When you consider the potential money savings, GAP coverage is a no-brainer.

See how much full protection could cost you – Build a GAP quote in seconds